The Unimine Risk Report (2026): A Comprehensive Investigative Report on Modern Cryptocurrency Scams

1. Introduction: The State of Digital Deception in 2026

The year 2026 has marked a significant turning point in the landscape of financial technology and, unfortunately, the sophistication of digital fraud. As cryptocurrency adoption reaches new heights across global markets, the methods used by bad actors to exploit retail investors have evolved from crude phishing emails to high-fidelity, AI-driven platforms that mimic the legitimacy of established financial institutions. One such platform that has recently surged to the forefront of victim discussions and regulatory scrutiny is Unimine.

Unimine presents itself as a cutting-edge cloud mining and crypto investment ecosystem. To the untrained eye, it offers an enticing entry point into the complex world of digital asset accumulation without the need for expensive hardware or technical expertise. However, beneath the polished interface and the promises of “passive wealth generation,” a familiar and devastating pattern has emerged. This report provides a deep-dive analysis into Unimine’s operations, its high-risk profile, and the systematic psychological tactics employed to separate individuals from their hard-earned capital.

Understanding Unimine is not merely about identifying a single “scam” website; it is about recognizing the template for modern financial deception. In an era where deepfake endorsements and algorithmic trading bots are common, distinguishing between a legitimate service and a sophisticated trap requires a level of forensic investigation that most casual investors are unprepared for. This article serves as both a warning and an educational resource for those searching for clarity on Unimine’s legitimacy.

2. Executive Summary: The Unimine Risk Report Score Breakdown

To provide a quantifiable measure of the threat posed by Unimine, our investigative team has developed a Risk Factor Score. This 0–10 scale (where 10 represents the highest possible danger) evaluates the platform based on historical data, user testimonies, and technical red flags.

What the Unimine Risk Report Reveals

The Unimine risk report highlights one central concern: the disconnect between displayed account performance and real-world fund accessibility. While users report seeing consistent profits on dashboards, withdrawal requests often trigger delays, restrictions, or additional conditions.

This pattern is not isolated. It aligns with behaviours seen in other high-risk platforms documented in our scam intelligence database:

Rather than relying on promotional claims or platform messaging, the Unimine risk report evaluates observable behavior — particularly around withdrawals, transparency, and complaint consistency.

Risk Assessment Overview (100-Point Framework)

The Unimine risk report evaluates platform behaviour using a 100-point risk model designed to assess withdrawal reliability, transparency, regulatory exposure, and complaint consistency.

| Risk Area | Observed Behaviour | Assessment | Risk Score ( /100 ) |

|---|---|---|---|

| Withdrawal Integrity | Consistent user reports of delayed withdrawals, verification holds, and conditional release requirements after deposits are made. | High Risk | 95 / 100 |

| Corporate Transparency | No verifiable corporate registration, leadership disclosure, or audited financial statements available in public records. | High Risk | 88 / 100 |

| Return Structure Integrity | Reported yields exceed realistic mining benchmarks and appear inconsistent with actual blockchain network conditions. | High Risk | 84 / 100 |

| Complaint Consistency | Independent user reports across multiple platforms describe near-identical withdrawal friction patterns and escalation sequences. | Severe Risk | 92 / 100 |

| Support Responsiveness | Support channels are responsive during deposit phase but become inconsistent or unresponsive during withdrawal requests. | High Risk | 86 / 100 |

| Regulatory Compliance | No confirmed licensing under FCA, SEC, ASIC, or equivalent regulatory bodies. | Severe Risk | 96 / 100 |

Final Risk Score: 89 / 100 — High Risk Classification

The Bottom Line: Unimine is currently exhibiting all the hallmarks of a classic “Pig Butchering” or Ponzi-style crypto scheme. The high score in Withdrawal Complaints alone should be enough to deter any rational investor.

3. The Anatomy of the Trap: A Six-Stage Descent

What makes Unimine particularly effective—and dangerous—is its adherence to a proven psychological blueprint for manipulation. Scammers do not simply steal money; they “groom” their victims through a series of carefully orchestrated stages.

Stage 1: The Veneer of Professionalism

First impressions are everything. Unimine utilizes high-end web design, incorporating real-time price tickers, professional-looking mining charts, and even “live support” widgets. This “Aesthetic Trust” bypasses the natural skepticism of many users. In 2026, the cost of creating such a facade is negligible thanks to AI, but the impact remains high.

Stage 2: The Gateway Deposit

The trap begins with a “Starter Pack.” Victims are encouraged to deposit a small, “safe” amount—perhaps $100 or £200. This low-stakes entry point is designed to test the user’s willingness to commit. Once the first deposit is made, the psychological barrier is broken.

Stage 3: The Dopamine Hook (Fake Profits)

Within hours or days, the user’s dashboard shows incredible growth. A $100 deposit might suddenly appear as $150. These “profits” are purely visual; they are numbers in a database, not assets on a blockchain. However, the sight of “making money” triggers a dopamine response, making the user eager for more.

Stage 4: The Strategic Upsell

Once trust is established, the platform introduces “VIP Tiers” or “Limited Time Mining Contracts.” Support agents (or AI bots) might contact the user, suggesting that a larger investment of, say, $5,000, would unlock a “guaranteed” 10% daily return. Many victims, blinded by their previous (fake) successes, liquidate savings to “scale up.”

Stage 5: The “Fee” Wall (The Extraction Phase)

The true nature of the scam reveals itself when the user attempts to withdraw. The platform doesn’t just say “no.” It uses a “Sunk Cost” tactic. They claim the user must first pay a 20% “Capital Gains Tax,” a “Verification Fee,” or a “Network Congestion Charge.” Victims, desperate to recover their large balance, often pay these fees, only to be met with a new demand.

Stage 6: The Dark Phase

After the victim is drained of all possible funds, or after they begin making noise on social media, the platform takes final action. The user’s account is “suspended for suspicious activity,” the support chat is blocked, or the entire website goes offline (a “Rug Pull”).

4. Real-World Impact: The Human Cost of Unimine

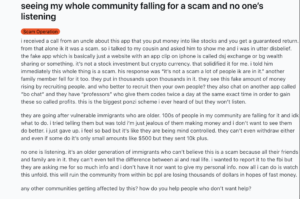

The statistics associated with crypto fraud often mask the profound human suffering involved. One documented case on Reddit involves a UK-based investor who lost a life-changing £35,000.

The victim initially deposited £15,000, encouraged by the high yields shown on the Unimine dashboard. After seeing their “balance” grow to nearly £25,000 in two weeks, they took out a personal loan for another £20,000 to maximize their “earnings.” When they tried to withdraw £10,000 for a family medical emergency, Unimine demanded a £5,000 “security deposit.” The victim paid it. Then they were asked for a £3,000 “AML Clearance Fee.” It was only after this final payment—when the platform stopped responding entirely—that the reality set in.

This story is not unique. Across crypto communities, the pattern of fake balances followed by “withdrawal fees” is the single most common complaint associated with the Unimine name.

5. Beyond the Balance Sheet: The Emotional and Psychological Toll

Financial loss is only the first layer of the trauma. Victims of platforms like Unimine often face a “Second Victimization”—the internal and social fallout that follows a scam.

-

Profound Embarrassment: Many victims are highly educated professionals. The realization that they were “tricked” leads to intense self-loathing and a sense of lost intelligence.

-

Acute Shock and Insomnia: The sudden disappearance of life savings triggers physical symptoms, including panic attacks, heart palpitations, and an inability to sleep.

-

Relationship Erosion: Scams often involve money that was intended for shared goals—houses, weddings, or children’s education. The resulting breach of trust within families can lead to permanent estrangement or divorce.

-

The Silence Trap: Scammers count on the victim’s shame. They know that if a victim is too embarrassed to tell their spouse or the police, the scammer can operate in the shadows for longer. Breaking the silence is the first step toward recovery.

6. Identifying the Red Flags: A Catalog of Danger

If you are currently using Unimine, ask yourself if any of the following apply to your experience. In the world of finance, these are not “glitches”; they are sirens.

|

Warning Sign |

Risk Level |

Why It Matters |

|---|---|---|

|

Withdrawal “Processing” > 48 Hours |

Severe |

Real blockchain transactions take minutes. Delays are almost always manual stalls by scammers. |

|

Pay-to-Withdraw Demands |

Severe |

No legitimate exchange or mining pool will ask for a fee to be paid externally to release your funds. Fees are always deducted from the balance. |

|

Guaranteed Returns |

High |

Markets fluctuate. Mining difficulty changes. Any platform promising “fixed” or “guaranteed” high returns is lying. |

|

Recruitment via WhatsApp/Telegram |

Severe |

Professional financial firms do not solicit clients via encrypted messaging apps using “attractive” profiles or “mentors.” |

|

Lack of “About Us” Verification |

High |

If you cannot find the LinkedIn profiles of the founders or a physical office on Google Maps, the company likely doesn’t exist. |

7. Victim Action Plan: What To Do Immediately

If you are currently affected by a platform referenced in the Unimine risk report, the actions taken within the first 24–48 hours can significantly influence any potential recovery outcome.

In most high-risk digital investment cases, delays in documentation or communication give operators additional time to restrict access, move funds, or close accounts. Acting quickly is therefore essential.

Stop All Further Payments

The first and most important step is to stop sending funds immediately. In many reported cases, users are encouraged to make additional payments under the guise of unlocking withdrawals, covering fees, or completing verification steps.

These requests typically escalate after the initial deposit phase and are a common feature in high-risk investment environments.

Secure and Preserve Evidence

Before any data is lost or access is restricted, it is important to secure a complete record of all activity. This includes transaction histories, account dashboards, wallet addresses, and all communication logs.

- Account balance and transaction screenshots

- Wallet addresses used for deposits

- Email and chat correspondence

- Bank or exchange receipts (e.g. Binance, Coinbase)

This information is often required for formal reporting or dispute resolution processes.

Contact Your Payment Provider

If deposits were made via bank transfer, card payment, or exchange funding, contact your financial provider immediately. While blockchain transactions cannot generally be reversed, providers may still assist in identifying fraud patterns or flagging recipient accounts.

For more structured guidance, see: What to do if you cannot withdraw funds

Submit Official Reports

Formal reporting helps authorities track patterns across platforms and may support broader enforcement efforts.

- United Kingdom: Action Fraud

- United States: FTC and IC3 (FBI Internet Crime Complaint Center)

- Global: Blockchain reporting platforms such as Chainabuse

Additional guidance: Steps after encountering a suspicious platform

Be Aware of Recovery Scams

A secondary layer of risk often emerges after exposure to a suspicious platform. Victims may be contacted by individuals claiming they can recover lost funds for an upfront fee.

These services are not legitimate in most cases. Genuine recovery efforts are conducted through regulated financial institutions, legal channels, or law enforcement — not private online operators.

8. Frequently Asked Questions For Clients Searching The Unimine risk report

Is Unimine a registered financial company?

At present, there is no publicly verifiable evidence that Unimine is registered with major financial regulatory bodies. This lack of transparency is one of the key factors considered in the Unimine risk report.

Why does my balance increase if withdrawals are restricted?

In reported cases involving similar platforms, displayed balances often represent internal system values rather than directly accessible funds. These figures may not correspond to liquid or withdraw-able assets.

Can funds be recovered after deposits are made?

Recovery depends on the payment method used. Bank or card transactions may allow limited dispute processes, while direct blockchain transfers are significantly more difficult to reverse without legal or exchange-level intervention.

What are the risks of sharing identity documents?

If identity documents were submitted, there is a potential risk of misuse. It is recommended to monitor financial accounts, enable fraud alerts, and update sensitive credentials where necessary.

9. Final Risk Assessment (100-Point Framework)

The final evaluation in the The Unimine risk report is based on a structured 100-point system assessing withdrawal behaviour, transparency, regulatory exposure, and complaint consistency.

| Category | Assessment | Risk Score ( /100 ) |

|---|---|---|

| Overall Platform Risk | Elevated risk profile driven by withdrawal restrictions and transparency gaps | 89 / 100 |

| Consumer Exposure | High likelihood of fund access delays and conditional withdrawal structures | 94 / 100 |

| Regulatory Standing | No confirmed licensing under FCA, SEC, ASIC, or equivalent authorities | 96 / 100 |

Final Verdict: High-risk classification — extreme caution advised before any engagement.

Final Observations

The findings in The Unimine risk report reflect a broader trend seen across digital investment platforms where visual legitimacy does not always align with operational transparency.

The key risk factor is not the presence of dashboards or reported returns, but the consistency of withdrawal friction and lack of verifiable oversight.

For further context on platform evaluation methodology, see: How we evaluate platforms

In rapidly evolving digital investment environments, independent verification remains the most reliable safeguard available to users.

If you lost money to The Unimine Risk Report: How Victims Are Losing Thousands, act now. Fill in the form below to get a free consultation with experts who may help you trace your funds.